The third flotation of the Egyptian pound : the roots of the crisis and the prospects for interaction

This paper discusses the economic roots of the recent Egyptian decision to float the pound, and its depreciation against the US dollar for the third time in six years to reach an unprecedented level. The paper concludes that the step is not feasible to reform the economy, due to structural problems that must be addressed.

As was expected, and near the anniversary of the painful devaluation of the pound, in early November 2016, Egypt implemented a new devaluation, the second in one year, and the third in only six years, which is known in the media as the flotation, that is, leaving the pound to the free market and the mechanisms of supply and demand; Which is belied by the successive large doses of devaluation, which confirm the reality of managing – and trying to curb – the exchange rate as an inevitable for an economy in the conditions of the Egyptian economy, which suffers from chronic trade and resource deficits, the accumulations of which force it to devalue the currency periodically to reset its nominal exchange rate with its real exchange rate; To ensure the stability of transactions and the movement of capital, as well as curbing tendencies to hoard currencies and speculate on them…etc.

In fact, what we see is not new as a general trend, but rather is closer to an explicit historical trend for more than five decades at least, but what is remarkable is the increasing acceleration with time, while it took almost three decades from the beginning of World War II until the setback of June 1967 The dollar barely doubled against the pound once, with the latter dropping from 20 piasters to the dollar to 38 piasters. It took only about one decade to double again, with the pound dropping from 40 piasters to the dollar to 83 piasters during the period 1978-1990, after which the pound started A series of collapse, with a rapid drop to three pounds to the dollar in just three years at the end of 1993, with the implementation of the economic reform program implemented by former President Hosni Mubarak, to continue on this path of ranging between short periods of stability, and jumps down with currency crises. Renewed, to the end of the story known as Three Floats, in common terms, in Six Yearspast.

This acceleration since the seventies indicates the emergence of other factors that aggravated the original trend. What are the roots of the original trend? And what are those factors that make this frequent decline necessary or inevitable in this way? It is certain that the successive Egyptian governments do not antagonize the people and do not like to incur their anger against them by these measures, and it is also certain that they are not the result of natural disasters beyond their responsibility. Depreciation of the pound over the past half century.

The qualitative underdevelopment of an underdeveloped economy

Since the 1970s, industrialization has receded in favor of unproductive service upheaval; To form a semi-industrial economic model that is unsustainable in general, and for a country the size and population of Egypt in particular, that suffers from continuous fluctuation in overall growth rates, due to the great exposure to resources and rentier practices that have gained an influential position in the economy, but within a general trend of decline over five decades with a decline in These resources are at the level of the region as a whole, while dominated by a sectoral composition that expresses the well-known standard course of the Dutch disease resulting from that rent-seeking tendency; Where the commercial commodity sectors declined, i.e. the manufacturing industry and agriculture capable of exporting abroad, in contrast to the growth of the local non-commercial sectors such as construction, trade and services. The manufacturing industry showed great volatility, but within a general stagnation it remained stable with it at an average of about 17% of the total output that was Accordingly, with the beginning of the opening period, agriculture declined without much improvement in the economy productivity, even closer to stagnation and a growing food gap; What appears is that it continues to employ at least one-fifth of the workforce.

These trends were reflected in the qualitative decline of the economy, that is, its simply backwardness, as shown by the Economic Complexity Index (1) , which estimates the degree of development of the economy through the extent of its commodity and sectoral diversification, with Egypt’s lagging position in 69th place out of a total of 133 countries covered by the index globally in 2020. It improved from rank 75 in 1995, and from the peak of its diversified decline in rank 81 in 2005, all of which belong to the lower half of the index, i.e. below the global economic average in general.

Commercial underdevelopment of the non-development economy

While Egypt is ranked 57th in the world in terms of export, it is ranked 41st in terms of import; To be in the sum in position 123 of 127 from the side of the trade balance (2) ; This reflects the chronic negative gap between merchandise exports and imports, with imports reaching three times the exports sometimes, and even after forty years of applying openness policies, exports covered only about a third of imports. Qualitatively, oil exports represented about 40% of the total merchandise exports as an approximate general average throughout the last half century, and even reached about 75% of them in the early eighties, while high-tech commodities barely exceeded 340 million dollars in 2020, which is equivalent to only about 3% of exports Manufactured goods, already meager.

As for the terms of trade exchange, they in turn deteriorated as a logical result of this qualitative decline in exports. By taking the year 2000 as a base year with a hypothetical value of 100, the net terms of trade index for Egypt declined from 220, in 1981, to 94.8, in 1989, when Egypt was on the verge of Bankruptcy, to regain some of its loss, and to settle at an average of 150, since 2008 until today (3) , meaning that Egypt’s commercial position in the global economy today is worse than it was in the early eighties.

In general, the balance of payments adopted a general rule on addressing the trade balance deficit with a surplus of services, through resources with mainly rentier assets and nature, what was specifically known as the Big Four, namely, remittances of workers abroad, revenues from oil exports, Suez Canal fees, and tourism revenues, some of which are historically accidental and some of them are accidental Relatively stable, but all of them are volatile and unstable returns, highly affected by political and international conditions outside the control of the country; What resulted in a fragile balance of payments, financing basic needs necessary for the stability of the economy and the satisfaction of basic social needs, with limited and unstable rentier resources; Which made him vulnerable to regional and geopolitical fluctuations and to the brink of impotence all along; Recurring with it the financial crisis and the country’s resort to seeking foreign aid, as well as the increasing loans with their known risks.

Investment stagnation in the non-development economy

The overall investment in Egypt has declined since the state’s role in productive investment has declined; As a result of the decline in public investment without corresponding compensation from private investment, most of which was funded; For the aforementioned non-developmental nature, for the light consumer industry sectors, the service sectors, and rentier hoarding activities in general, and even the public investment itself contributed to encouraging that trend, and attracting more private investment behind it in that way, by ignoring the commodity productive sectors, and its intensive participation in those non-commercial sectors, This amounted to the explosive growth of the construction and building sectors and real estate activities, which amounted to 225% and 952%, respectively, during the period 2010-2017 4.

The paradox is that this trend of misallocation of public investments and real estate and service bias as a manifestation, after their initial quantitative reduction, is not separated from the essence of the development strategy promoted by international organizations, the IMF and the World Bank, which is mainly focused on withdrawing from any real productive activity, no matter how necessary, and focusing investment the public in infrastructure – within which the real estate sector is, of course – to attract foreign investment and encourage local private investment; For the Egyptian government to put tens of billions of dollars into new roads, bridges, and cities; Its outcome was an illusory numerical growth in GDP, compared to more than 121 billion dollars in new foreign debts that Egypt has incurred in the last ten years, bringing its foreign debts by more than 350%, from 34.4 billion dollars in 2012, to 155.

The chronic indebtedness of the non-development economy

Thus, the trade and investment resource deficits came together; In order to pay for escalating borrowing, we note its recurrence in the last half century, in the eighties in particular, and in the last decade following the January revolution; Where the current Egyptian administration copied the economic policy of the first decade of the Mubarak administration, stemming from the same problem of the development strategy promoted by the aforementioned international organizations, centered on developing infrastructure by borrowing, which is almost all the work of the World Bank, which paves the way with this strategy of repeated failure to attend his brother, The Monetary Fund, the owner of the famous conditionality, when the victims who entered the trap reach or are close to bankruptcy, as happened with Egypt in the late eighties, and as is happening today with a strange repetition of mistakes.

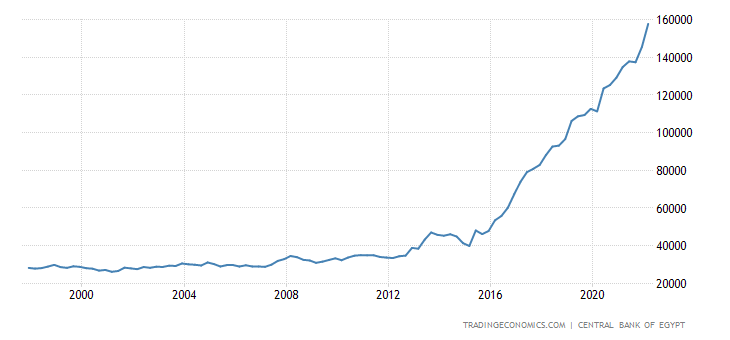

Just as Egypt’s foreign debt has multiplied several times over the past decade, Egypt’s foreign debt has escalated during the late seventies and throughout the eighties, jumping from 24% of the total national income in 1974 to 107% of it in 1981, to slow down a little and then jump to its historical peak at about 133% of national income in 1988 (6 ).

Prior to the debt rescheduling of the Paris Club agreements in the early 1990s, the ratio of short-term external debt to total reserves had reached catastrophic rates of 400% and 316% in 1986 and 1989, and to stabilize over the next two decades at very good ratios, reaching a maximum of 30% in 2000, and a minimum of 6.6% in 2006, to show upward tendencies over the last decade, until it reached 50% in 2016 before devaluing the pound at the end of the year, and after a relative decline for only two years, it rebounded to reach 30% in 2020 according to the latest available official data (7) , but it is sufficient in light of our knowledge With the local and global economic conditions, as well as the context of the Corona period and its aftermath, to know the general trend, which is supported by the strange secrecy of official statistics recently.

In fact, this state of public debt is rooted in the non-developmental character that dominates the economy, which makes it indebted by nature. However, the mentioned development strategy, which is not actually developmental, and is reinforced by the cosmetic tendencies of the Egyptian administrations, the abyss of the national show projects (8) , to multiply the dimensions of that situation and accelerate with its explosions; to put the Egyptian economy on the verge of bankruptcy; He is forced to negotiate anew with the sponsors of that strategy, pawn his local policies, sell his historical assets, and, of course, reduce his national currency.

About the pound: position and expectations

Thus, we find that the current commercial status of the Egyptian economy makes it an economy with a deteriorating international exchange rate, and even what appears to be stability since the early 2000s, is a product of, and an expression of, its general stagnation and qualitative decline as exports and imports in general, while its imports are a considered part of them necessary just because functioning at its present level, without any renewal or extended growth; which means its inflexibility; Hence, the trade deficit will persist in the foreseeable future. Similarly, the financial position – meaning the economic surplus – is characterized by its production of quantitatively deteriorating saving and investment rates, and poorly allocating qualitatively. Consequently, it suffers from an increasing investment resource gap; It leads to either new debt or more stagnation, especially if the country does not attract new foreign investment, to at least medium-term real productive employment.

As for the direct level of the current crisis, the stability of the pound in general is conditional on the stability of the indebtedness at safer limits; This means, in principle, the necessity of a short-term decrease in them, especially from its current level, which may not be high in relation to the total output, but it remains so for the available reserves, and in light of the limited and volatile sources of foreign exchange, which the general context and the dominant trends in it globally and regionally suggest its deterioration or stagnation. perfect.

All of this means, as a general conclusion, that from the strategic point of view, the Egyptian economy, with its current business model, needs increasing resources just to stay in place, that is, simply not to deteriorate, and from the tactical point of view, the pound will not stabilize in the short term unless the short-term debt ratio returns to its safe limits, At which time the economy can return to its normal working condition without great pressure on the limited reserves, and without this by excessive or exceptional restraint of the necessary imports in a way that hinders production at its usual level, as has been the case for several months.

Regardless of the fact that the issue of currency valuation is not without political calculations and the agreements of the elders; As one of the qualitative prices of the external debt and the weakness of national independence, we cannot trust the expectations put forward regarding the level of stability of the pound at specific numbers against the dollar, especially with the current abnormal state of the economy, in terms of import restrictions and others, as well as the absence of transparency about a lot of information regarding final levels. Current total and short-term debt. But in general, and in light of the announced data, it is not likely to depart much from the current level, after the pound lost more than half of its value in just seven months.

By looking away to a broader time horizon, the reference scenario, i.e. assuming the continuation of the existing model economically and politically, inevitably leads to the continuation and repetition of doses of currency devaluation every few years at best, although more likely, assuming a minimum level of rationality, is the direction of some partial review of current policies , in particular the policy of excessive external borrowing; As the model began to show tendencies to accelerate the recurrence of crises in a way that threatens its entire stability.

Economic and social effects of devaluation

The most prominent of these effects can be summarized in the light of the Egyptian economic structure, and on the basis of the previous historical experiences of Egypt, in several basic effects from the short to the long term, as follows:

First : The exposure of the illusory growth of indebtedness over the past several years, with the immediate contraction in the GDP at least as much as the decline in the currency, and regardless of the other quantitative and qualitative effects on growth, which means its initial decline from the current level of 410 billion dollars (7.9 trillion pounds at a dollar price). 19.25 pounds, the first of last September) (9) , to 326 billion dollars in the blink of an eye (at a price of 24.20 pounds, the end of last October), repeating the same pattern when it decreased from 332 billion to 236 billion after the first flotation in 2016 (10) .

Second : A large inflation wave, which is likely, with the current global data, to exceed those that followed the 2016 float, which exceeded 30%, in 2017 (according to conservative official figures), although commodity prices have actually translated the current dollar price some time ago, and before the official reduction was made. The same, however, the monopolistic structure of the Egyptian market, with the large number of trading and brokerage rings, as well as the necessary adjustments in prices and wages just to keep up with the legitimate and fair new values, with the sectors that are late in adjusting their economic and market values, will collectively push for the continuation of the inflationary wave, even assuming the government’s success in restoring Confidence in the pound and ensuring the stability of the exchange rate against further depreciation in the short term at least.

Third : The state of stagnation, i.e. stagflation in general, deepens, with the rise in costs, the forced hike in interest rates, and the disruption of price structures; In general, the state of uncertainty and poor clarity of vision aggravated for at least several months; In a way that reduces new and real investment in particular, increases idle energies, and enhances the tendency to hoarding and speculation, in addition to the negative effects that all of this has on the fronts of the general budget, the prices of consumer goods, production requirements, and imported capital goods. Which weakens the group’s economic performance and financial indicators.

Fourth : the contraction of consumer demand, the largest source of economic growth in Egypt; What it means is the exacerbation of the stagnation situation, the decline in employment, the slowdown in many sectors and productive activities, and the high unemployment rates; As a consequence, the investment demand – which is already in crisis – weakens with it.

Fifth : A conditional relative improvement in the trade balance, but in a limited and temporary percentage in general, as demonstrated by the historical experience of previous floats, and for fundamental reasons that we will explain later.

Sixth : Possible rise in stock exchange indices; To compensate for the market values of the shares, it is initially just a nominal rise compensating for the decline in the exchange rate, and it can develop into a real rise by attracting new Arab and foreign liquidity with the attractiveness of the new exchange rate, although there is no guarantee that the scenario of the great rise of 2016 will be repeated, with the different international economic and political circumstances And the general downward trend of global financial markets, which is reinforced by the current US monetary policy.

Seventh : The low standard of living, high rates of poverty, and worsening of the misdistribution of income in favor of the asset-owning groups at the expense of the working groups. For example, the 2016 floatation wave led Egypt to advance on the global misery index from the eighteenth place globally in 2015 (11) to the fifth globally In 2016 (12) , with the shift in the main source of misery over the aforementioned two years from unemployment to consumer prices, which leads us to be more pessimistic with the current wave, with expectations that the exacerbation of unemployment will coincide with the rise in inflation, within the case of stagflation referred to above, and in the context of the economy The world is generally more tense.

Eighth : the instability of the currency exchange rate; What distorts all prices and weakens the incentives for positive savings and productive investment in general, and deepens the tendency to the rentier, service and light consumer sectors with quick returns; This deepens the nature of the non-productive rentier tendency, the deeper source of the crisis, and increases the weakness of confidence in the currency in general. which may lead to more compactness and dollarization; The state loses its monetary sovereignty and the effectiveness of its related policies, and the process of the national currency losing its functions gradually worsens, starting with the function of the store of value, then the function of the unit of account and forward exchange, until it almost ends with the loss of the function of the exchange medium itself.

Ninth : The loss of monetary sovereignty leads to the completion of dependency episodes, and the national inability to control resources, assets and the movement of capital deepens, as well as the renewal of independent self-production; This reinforces the essence of the economic crisis by perpetuating the state of dependency and underdevelopment.

Closing Comment: What about the benefits of a currency devaluation?

At the theoretical level, a traditional claim emerges of urgent economic advantages of currency devaluation, most notably that it, first, reduces the balance of payments deficit by lowering the relative prices of exports; By increasing them in quantity and total returns, in return for raising the relative prices of imports; In order for the opposite to happen, the final trade deficit will shrink accordingly, and secondly, it will fix price distortions in a way that improves the allocation of economic resources; It raises allocative efficiency and consequently economic growth.

The problem of this perception, like all perceptions of neoliberal economic ideology, is a leap over the reality and character of industrial backwardness that we discussed at the beginning of the paper as a decisive determinant of the nature and logic of the work of the Egyptian economy. and then measure it on the fundamentally different advanced industrial economies; What is the imaginary result of these expectations, or the limited realistic profitability at best; First: The relative price changes of the exports and imports of a semi-industrial economy such as Egypt’s are not sufficient to change them quantitatively to the degree necessary to bring about a significant and qualitative change in its trade position. Because there are other more important factors that affect it, most notably the extent to which the production apparatus is able to increase the supply of exports by imposing an increase in demand for them, and the extent of flexibility and the possibility of reducing or replacing imports; Either due to its lack of necessity or the ability to replace it with a local alternative.

Second: Flotation will not succeed in producing its effects except by curbing private consumption with its negative effects on economic growth, specifically for the middle and poor classes who are most affected by inflation. Because it is in fact a kind of historical debt repayment over time, but with an unfair distribution of its burdens.

In sum: regardless of the inadequacy of the policy of total flotation in general for an economy with the conditions of the Egyptian economy, it is not possible for a devaluation of the currency – as we must call it – to be in itself a real prelude to reform, especially with the huge economic and social costs to it, and the huge negative difference that Between potential limited gains and huge near-certain losses.

More importantly and more generally, it is awareness of the extremely dangerous indicators that this rapid repetition of the currency devaluation three times in only six years bears about the extent of the imbalance in the entire Egyptian economic system and the inefficiency of its general system of policies, as well as about the worrying trends for the future of the economy if they continue. What necessitates a comprehensive review based on the awareness that the economy needs a radically different path.

About the author

Magdy Abdel Hadi

Economic Researcher.REFERENCE

1-Egypt, The Atlas of Economic Complexity, (Viewed in 30/10/2022): https://atlas.cid.harvard.edu/countries/68.

2-Egypt: Trade Statistics, globalEDGE, (Viewed in 30/10/2022): https://globaledge.msu.edu/countries/egypt/tradestats.

3- Net barter terms of trade index (2000 = 100) – Egypt, Arab Rep., World Bank: https://data.worldbank.org/indicator/TT.PRI.MRCH.XD.WD?locations=EG.

4 “Study: More than 29% of housing units in Egypt are closed,” Hani Mohamed, Akhbar Al-Youm, Cairo, June 29, 2019, (access date: October 31, 2022): shorturl.at/clAZ4

5-Egypt Total External Debt, Tradingeconomics: https://tradingeconomics.com/egypt/external-debt.

6 –External debt stocks (% of GNI) – Egypt, Arab Rep., World Bank: https://data.worldbank.org/indicator/DT.DOD.DECT.GN.ZS?locations=EG.

7-Short-term debt (% of total external debt) – Egypt, Arab Rep, World Bank: https://data.worldbank.org/indicator/DT.DOD.DSTC.IR.ZS?end=2020&locatio….

8 Magdy Abdel Hadi, “The Egyptian Economy.. Cosmetic Projects as an Alternative to Structural Development,” Al Jazeera Center for Studies, Doha, November 30, 2021, (access date: October 31, 2022): https://studies.aljazeera .net/ar/article/5214 .

9 Egypt announces a rise in GDP to 7.9 trillion pounds, arabic.news.cn, September 3, 2022 (entry date: November 1, 2022):

http://arabic.news.cn/20220903/c72a544af4c64904a01409bad9549558/c.html

10-GDP (current US$) – Egypt, Arab Rep., World Bank: https://data.worldbank.org/indicator/NY.GDP.MKTP.CD?locations=EG.

11-Amanda Macias, The 29 Most Miserable Countries In The World, Business Insider, 23/1/ 2015 (Viewed in 1/11/2022): http://www.businessinsider.com/the-29-most-miserable-countries-in-the-w….

12-Steve H. Hanke, The World’s Most – And Least – Miserable Countries in 2016, Cato Institute, 17/1/2017 (Viewed in 1/11/2022): https://www.cato.org/blog/worlds-most-least-miserable-countries-2016.