Aviation Industry & National Security in Europe (2020-2021)

By Amr Samaha - The Egyptian Center for Strategic Studies

")

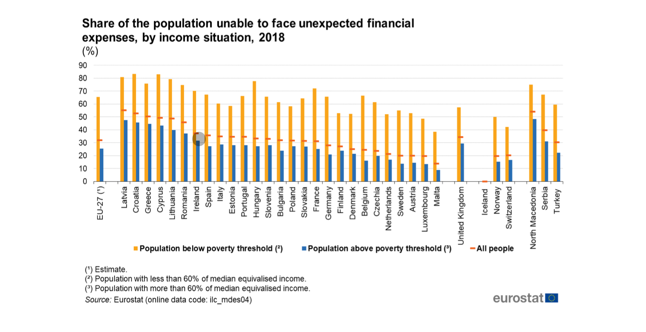

COVID-19 pandemic had a devastating effect on the aviation industry globally in 2020, changing the aviation connectivity map. European Union has still been struggling economically since the 2010 economical crisis, with 3 of its members states having more than 50% of their population unable to pay for unexpected financial expenses, and many others recording more than 40% of their population unable to. Europe economy has been severely impacted by the pandemic as one of the most unregulated free markets for the aviation industry world-wide, which implemented many free-market treaties to ensure fair competition and to encourage capital funding. European governments has for the last 6 month been hassling to bail out their once national airlines, dumping billions of dollars into the industry, not only to save jobs and prevent economical breakdown of the industry, but more important is to preserve their EU national security.

National security according to the Europe commission or newly called European sovereignty focuses more on a nationalist agenda shifting from a more globalist one, which takes into account many challenges, focusing greatly on economical and financial aspects of the union as one of its main concerns. Aviation plays a crucial role in the Union’s economy and in the everyday lives of European Union citizens, and is one of the best performing and most dynamic sectors of the European Union economy. EU airlines face liquidity challenges due to COVID-19 pandemic and massive cash burn, its affecting EU economy negatively affecting millions in different sectors. Aviation industry directly contributes by $300 billions into European GDP, supporting an estimate of 5 million jobs, which is about 2.1% of European GDP. Moreover, the industry has a massive positive indirect contribution to European economy, affecting as much as its direct effect. Aviation sector directly & indirectly contributes by $823 billions to European economy, supporting 12.2 million jobs, which is around 3.3% of total employment and 4.1% of GDP in all of Europe.

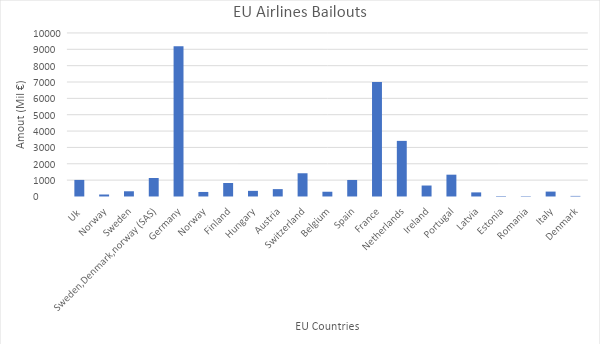

Supporting the aviation industry from economical collapse is a worldwide security concern especially in Europe. European airlines bailout hit €26.6 billion in assistance to the continent airlines post COVID-19. This amount ranges to around 46% of European airlines capital pre-pandemic, showing how serious the European government is willing to invest in order to ensure European aviation survival and ability to compete post pandemic.

Pumping liquidity into collapsing airlines is not the only approach that is being taken by the European government to secure European aviation industry survival. An all-new approach some European governments are planning to implement post pandemic which opposes their free market ideology. A calculated short term partial acquisitions of Lufthansa & IAG, that German and British governments are planning to execute.

The British government has plans to take control and buy equity stakes into airlines affected by the pandemic, in-order to insure their survival. This step has been stated as it was unveiled that the government backed loans given to British airlines parent IAG alone as over £330 billion to bridge their liquidity and cash-flow gap caused by the pandemic might not be enough to support these collapsing airlines, which could lead to their bankruptcy. On the other hand, the German government which has sold its last 37.5% share in Lufthansa airline in October 1997 which at the time was the second biggest privatization deal in German history, has in last May agreed to support the company with a rescue package of €9 billion. Along side the rescue package is a strategic short term investment plan to buy back 20% of the company’s stake for €300 million, in which it plans to sell back by 2023 in an attempt to revive the airline and support it.

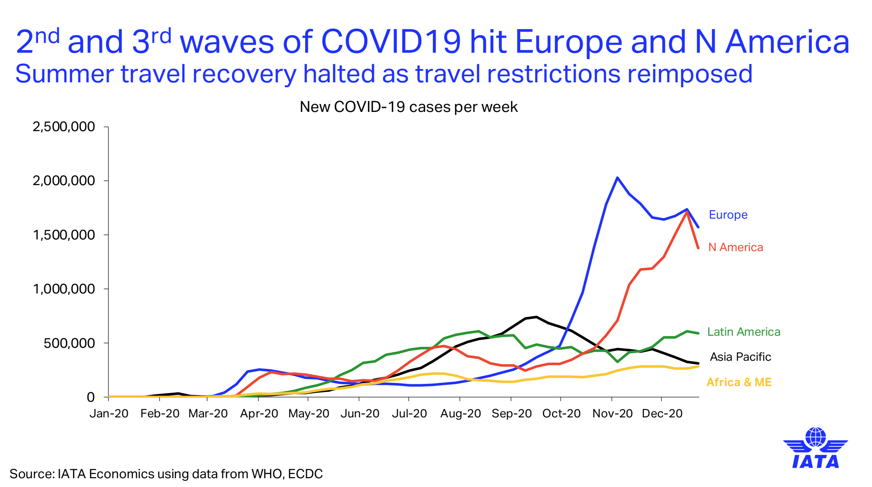

By the start on 2021 and with the second wave of COVID-19 hitting Europe and the emergence of a new strain of corona virus in the UK, a sharp decline in passenger seats and revenue is expected, which is shown and confirmed by the IATA’s latest projection showing a sharp decrease in number of passengers in Europe and North America as from January 2021. On the other hand ICAO’s latest projection for European airlines recovery which are based on 2 main recovery scenarios, scenario 1: nike swoosh and W-shaped, and scenario 2: U- and L-shaped, are of concerning outputs. ICAO projection states that in the best possible scenario European airlines could reach the same passengers revenue as that of march 2020 by the late June 2021, which widens the cash burn expected by most European airlines by another 5 to 6 months.

Extreme measures is expected to be implemented by the European governments to ensure the survival of their civil airlines as their loans and grants dry out. Negotiations of privatization plans and majority stakes being sold to governments will be negotiated on a broader range, which will include many small companies which will not be able to survive economically and won’t risk more loans to secure liquidity and more cash burns. More drastic steps could be taken against third operator countries, as to limiting tycoon airlines such as Qatar Airways, Emirates Airline and Etihad Airways from operating inside the European union or restricting their flight routes under false cover stories as to give European carriers a fighting chance. Such cover story restrictions was seen implemented by the US trump administration in late March 2017 under Flight security restrictions concerns on middle-eastern countries with the biggest flight carriers, but holding an absolute hidden agenda. These restrictions were implemented on middle-eastern airlines under a false propaganda cover just one month after the CEOs of 3 major US airlines have petitioned to US Secretary of State Rex Tillerson about their concerns of massive subsidization of state-owned airlines by Persian gulf nations which are affecting American jobs and eliminated US carrier services to the Middle-East and India.

The restrictions included all the major airlines in the Middle-East which were Egyptair, Emirates Airline, Etihad Airways, Kuwait Airways, Qatar Airways, Royal Air Marco, Royal Jordanian Airlines, Saudi Arabian Airlines and Turkish Airlines, which main aim was to pressure their governments to Abide by the partnership for open and fair skies concerns and cut of subsidies to their airlines. One of the main pillars that aviation industry is built on with no regards to politics or economics is safety. Lately EASA is considering to relax some rules that restrict single-pilot operations in commercial aviation. This new implications brings a lot of questions of pilot incapacitation procedures and worries stemming from the German-wings tragedy in 2015, as well as its difficulty to be implemented due to basic pilots physiological needs. Although this kind of operation compromises safety standards, it is still considered as it definitely benefits EU airlines economics tremendously in a time of crisis.

On 27 march 2019 in Brussels, the European Parliament has signed a regulation to safe guard the European carriers from unfair competition from third countries. This regulation was established in context with the Chicago conversation on international civil aviation in 1944 which acknowledged the need for international air transport to be established on the basis of equality of opportunity. Article 44 of the Chicago convention also states that the International civil aviation organization (ICAO) is responsible for the development of international air transport and ensure that every contracting state has a fair opportunity to operate its international airlines. On the hand, implementing bans on airlines which may cause a threat to European carriers operation in order to safe guard their survival might not be in Line with these legislations, except when they take a different cover (eg. Security, COVID, ..etc) will they be eligible. Grants, bail outs & loans guarantees given to EU airlines doesn’t stand in line with these regulations. European airlines gain tremendous advantage over other third countries operators whose governments might not not able to support their airlines at the present time by such huge budgets or has other priority fields to invest in post COVID-19.

In conclusion, fair competition, open markets & insuring equal opportunities for international air transport are regulations that are acknowledged and followed in the EU only when it benefits EU economical and political agenda. When EU national sovereignty is at risk, extreme measures are taken to preserve its well being, disregarding all international regulations that might be a factor in hindering its progress.